Death by a thousand cuts - when portfolios go sideways

- Noel Watson CFPᵀᴹ - Chartered Wealth Manager

- Dec 5, 2023

- 4 min read

Updated: Jul 10

Introduction

Maybe the blog title was slightly dramatic, but there's no doubt that retirement portfolios drifting sideways is currently one of the most frequently raised topics by our clients (and the clients of other financial planning firms we regularly speak to). In an ideal world, markets would trend smoothly upwards in a straight line. Of course, that is never likely to be the case all of the time; we are prepared to accept some volatility in our short-term returns in the expectation that the portfolio will generate longer-term returns to combat inflation over a multi-decade retirement.

This article examines recent market performance and how it might affect our clients' retirement plans.

Lifeboat drills

At Pyrford Financial Planning, we prepare clients for the inevitable sharp falls in their retirement portfolios, which they will periodically encounter, to ensure they stay the course and remain invested. We review historical market volatility during the initial onboarding process and schedule periodic refreshers.

Drifting sideways

These lifeboat drills haven't had to be used in recent years. Instead, the markets haven't really gone anywhere post-COVID rebound.

ARC returns for the last three years are shown below (see our evaluation of the "No-Brainer" portfolio for more on ARC). The more bond-heavy portfolios have tended to suffer more, with some showing negative performance over the period.

Am I going to be OK?

While our clients would prefer rising portfolios to those that are broadly flat, what they really want to know is:

"Does our portfolio performance over the last three years impact our retirement plans? Are we going to be OK?"

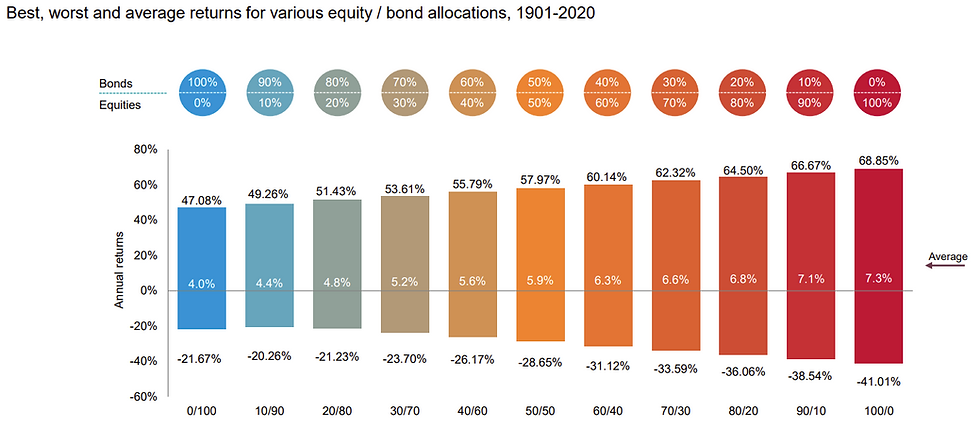

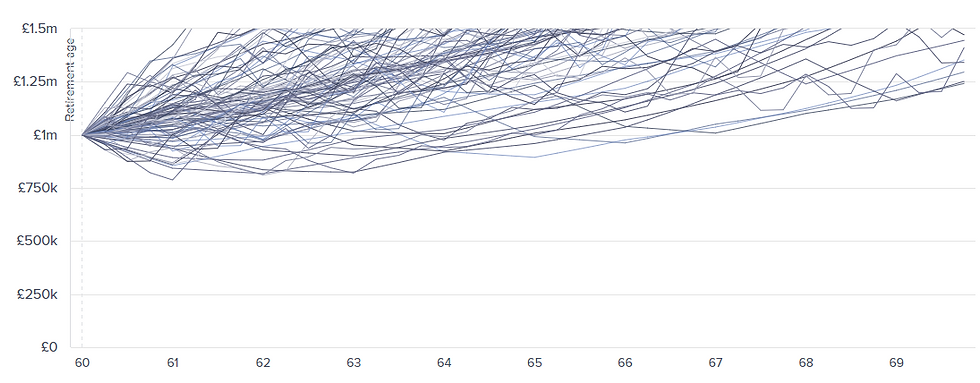

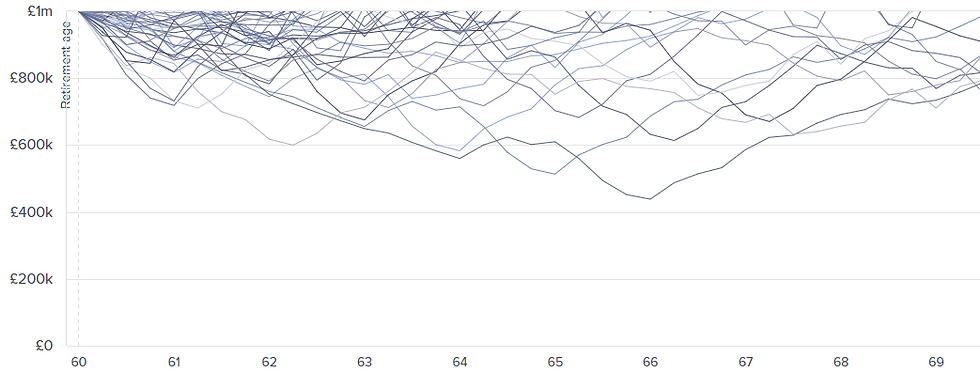

To investigate, we will use our favourite retirement planning tool, Timeline. We will use a global 60/40 portfolio with no fees or withdrawals (to analyse historical market returns rather than retirement sustainability). We can see that in many historical scenarios, the portfolio nominally has fallen from the starting balance of £1,000,000, in some cases quite heavily.

Our retiree, who finished work at the turn of this century, was almost 20% underwater in 2003 (the lost decade from 2000-2010 was a tough time for some equity investors).

Indeed, we can see our 1917 retiree only returning to their starting balance after around seven years!

"Ah, but that's nominal!" you may say. "We've had some terrible inflation over the last three

years".

The RPI All Items Index stood at 293.3 in October 2020, and three years later, it stood at 377.8, an increase of just over 28%. If we assume a portfolio worth £1,000,000 in October 2020 is now worth approximately £700,000 in real terms (flat in nominal terms) three years later, how does that compare to history? Similar to our nominal returns analysis, we can see significant falls in real returns over protracted periods.

Our 1916 retiree's pot would have fallen even further in real terms than our 2020 equivalent (£700,000 vs £655,000) over three years (although enjoying retirement during WW1 was far from a top priority during this highly challenging time).

A longer timeframe

While the last three years have indeed been challenging, it's fair to say we've seen worse. What if we expand our returns window to five years? The ARC data is more positive, with the portfolios all in positive territory.

In October 2018, the RPI All Items Index stood at 284.5, giving RPI inflation around 33% over the last five years. Assuming the typical portfolio is now worth around 25% less in real terms (a rise of 15% in nominal terms), giving an investment balance after five years of about £750,000 if the retiree had started with £1,000,000.

After six years, our 1916 retiree's pot had almost halved in real terms. Don't forget, this is without investment fees or withdrawing money from the investments. It's worth reading our blog post on the "4% rule," which covers this period in more detail.

Conclusion

While the last three years have not been great in terms of returns the markets have generated, there are several positives:

Our clients have stuck to the plan and remained invested. The behaviour gap (the difference between investment and investor returns) is very real and can dramatically impact client outcomes. Helping clients stick to the plan is a vital part of our job, and it's why we write articles like this.

It would be easy for us to agree to change portfolio compositions to placate clients (you'd be surprised how often we hear of this happening), at least in the short term, but our overriding priority is to help our clients achieve their objectives, even if it means having tough conversations.

The benefit of having access to historical data is that we can see that worse periods have been encountered than those we've had in recent years.

Our retirement plans are built to cope.

Inflationary periods can have a "double whammy" effect on the sustainability of a retirement portfolio. One example is the 1970s, where inflation remained high over the decade.

1. Retirement withdrawals tend to (broadly) increase with inflation, putting the retirement pot under more pressure.

2. Bond values tend to fall, reducing the balance for a typical portfolio.

Again, our retirement plans are built to cope.

Want to find out more?

Please get in touch with us if you want help building a robust retirement plan to cope with challenging market conditions.

About us

The team at Pyrford Financial Planning are highly qualified Independent Financial Advisers based in Weybridge, Surrey. We specialise in retirement planning and provide financial advice on pensions, investments, and inheritance tax.

Our office telephone number is 01932 645150.

Our office address is No 5, The Heights, Weybridge KT13 0NY.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Comments